by Mischler MarCom | Nov 26, 2018 | Debt Market Commentary, Recent Deals

Quigley’s Corner 11.26.18 : Dominion Energy VEPCO Debt Deal Distilled “From an ethical standpoint, serving those who sacrificed so much to serve us is the right thing to do.” – Thomas F. Farrell, II, Dominion Energy Chairman, President and CEO...

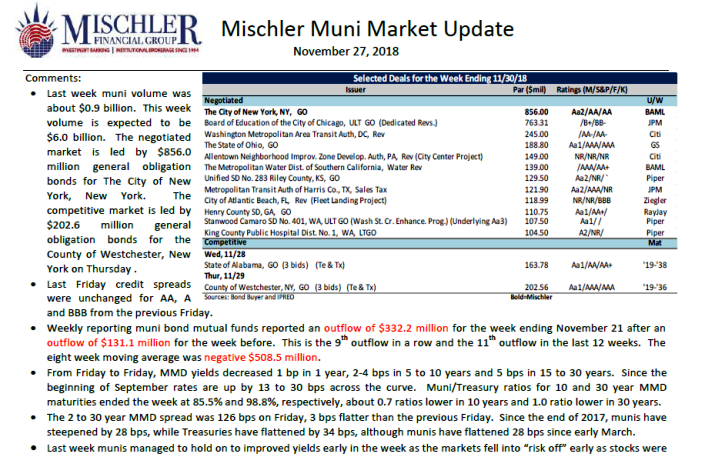

by Mischler MarCom | Nov 26, 2018 | Muni Market

Muni Market New Bond Offerings Scheduled for Week of November 26, 2018- A New York State of Mind…Mischler Muni Market Outlook provides public finance investment managers, institutional investors focused on municipal debt, and municipal bond market participants...

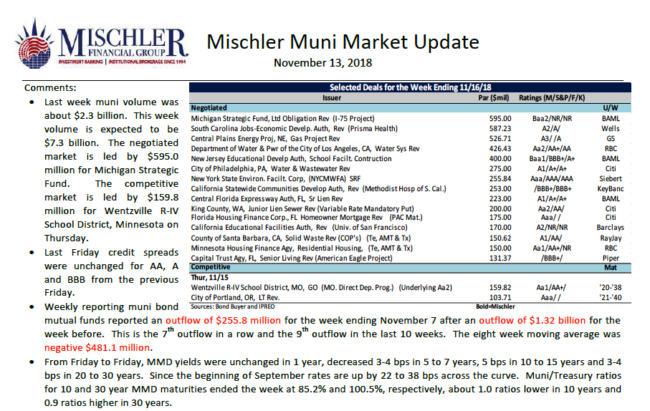

by Mischler MarCom | Nov 13, 2018 | Muni Market

Muni Market New Bond Offerings Scheduled for Week of November 13, 2018- Mischler Muni Market Outlook provides public finance investment managers, institutional investors focused on municipal debt, and municipal bond market participants with a summary of the...

by Mischler MarCom | Nov 9, 2018 | Debt Market Commentary

Quigley’s Corner Veterans Day 2018 Edition: Digging In For DowDupont Deal ALL POINTS BULLETIN – Calling All “QC” Readers: EEI Conference NOV 11-13 An important Veteran’s Day Announcement and Thank You! Investment Grade New Issue Re-Cap – “QC” Q&A Today’s IG...

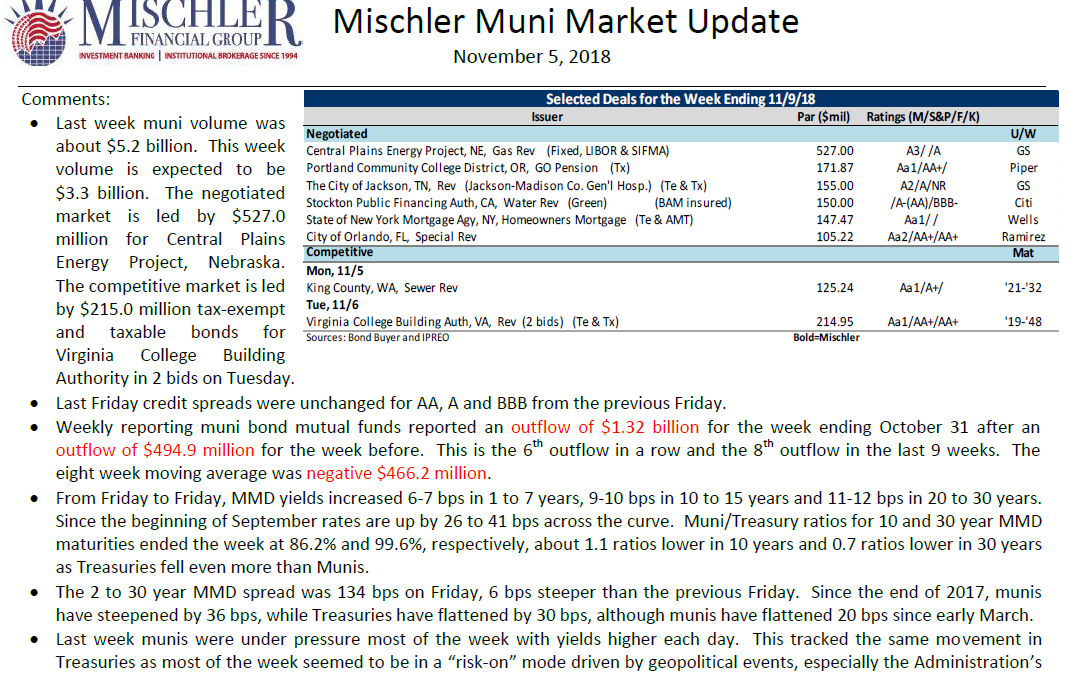

by Mischler MarCom | Nov 5, 2018 | Muni Market

Muni Market Debt Offerings Scheduled for Week of November 5, 2018- Mischler Muni Market Outlook provides public finance investment managers, institutional investors focused on municipal debt and muni bond market participants with a summary of the prior week’s...